One of the key questions buyers and sellers face in every M&A transaction is the tax planning, i.e. related tax implications. The tax consequences of M&A transactions vary considerably depending on the structure of the deal and the flexibility of the parties.

Tax implications are based on how the transaction is structured; for example, a stock/equity transaction has different tax implications than an asset transaction. Without proper consideration, there can be unintended consequences and unexpected costs. In this article we explore a tax structure that can be used to minimize the tax liabilities of international sellers of M&A stock transactions; however, we should emphasize the need for careful consideration when determining the route to take.

Hungary in International Tax Planning

Hungary is relatively rarely used in international tax planning, although it has a number of legal institutions that can be used extremely well in international tax planning. Moreover, it is a member of the European Union and the OECD and has concluded international tax treaties with nearly 100 countries.

One such useful legal institution is the reported shareholding. Its essence is that if a Hungarian (tax resident) company acquires a stake in another company (which may also be foreign one) and declares this acquisition to the tax authority and sells this share after one year, the profit made on the sale is tax-free. Since dividends paid to companies are not subject to withholding tax in Hungary, tax-free capital gains can be paid tax-free to the foreign corporate owners of the Hungarian company, regardless of its registered address.

Details

The concept of reported shareholding is defined in the Corporate Income Tax Act, according to which reported shareholding means a share acquired under domestic law in a legal person and/or a foreign person (except a controlled foreign company but including an increase in the percentage of the previously declared shareholding), provided that the taxpayer notifies the acquisition to the tax authority within 75 days of the acquisition.

It can be seen from that concept that a shareholding may constitute a declared shareholding if the following cumulative conditions are met:

— the taxpayer acquired the participation in a legal person constituted under domestic law or in a foreign person;

— the foreign person in which the shareholding was acquired is not a controlled foreign company;

— the shareholding does not constitute units issued by an investment fund with an indefinite duration;

— within 75 days of the date of acquisition, the taxpayer shall notify the acquisition to the tax authority.

It is important to note that, similarly to other cases of tax base adjustments, the tax base adjustment related to the declared shareholding is also subject to a pair of corrections in the Corporate Income Tax Act, the application of which depends on whether the taxpayer realized an exchange rate gain or a loss during the sale of the declared shareholding (this should also be considered during tax planning).

Losses recognised as a result of the derecognition of the declared shareholding on any basis (e.g. in case of sale, but also taking into account the expenses recognised as a result of the derecognition of financial goodwill) increase the tax base, in other words this cost is not accepted for CIT purposes. The amount of impairment recognised or reversed as an expense in recognition of an impairment also adjusts the tax base.

It can be seen that in the case of the derecognition of the shareholding on any grounds, the tax base adjustment (increase) must be taken into account if there is a loss on the shareholding, and this is true both within and beyond 1 year from the acquisition.

Reviewing the above, we can conclude that the legal institution of reported shareholding may provide a tax advantage in case of sale of shareholding for those who make a profit in the course of the transaction. This requires that the expected market value at the time of sale exceeds the book value of the shareholding. Of course, it is not easy to see how the future market value of a share will change, but with careful planning, it is not impossible.

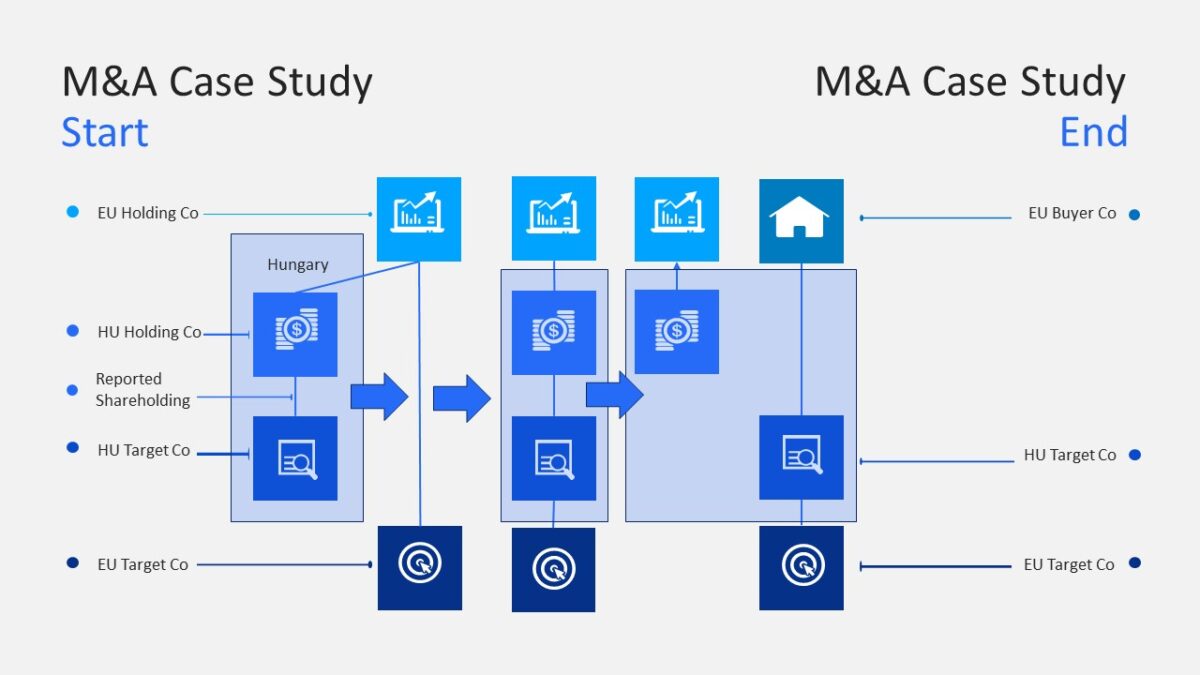

Case Study

A recent tax ruling issued by the Hungarian tax authority has made the above structure even more favourable and usable during tax planning. According to the ruling, changes in the ownership structure of the companies concerned by the reported shareholding do not affect the taxation of the reported shareholding: its sale will be exempt irrespective of the restructuring.

According to the background in question, a Hungarian taxpayer (HU Holding Co) acquired a 100% stake in another Hungarian taxpayer (HU Target Co) (which, however, could have also been a foreign company). The acquiring Hungarian company (HU Holding Co) had a foreign EU parent company (EU Holding Co), which also had other regional non-Hungarian subsidiaries (EU Target Co). There was a restructuring within the group, more than one year after the acquisition of HU Target Co, i.e. at the time when HU Target Co could already be sold tax-free by HU Holding Co.

The intra-group restructuring involved a foreign subsidiary (EU Target Co), which eventually became the property of HU Target Co and finally HU Target Co was sold to a buyer outside the group (EU Buyer Co). The profits from the sale of the reported shareholding in HU Holding Co was exempt from tax and the distribution of these tax-free profits to EU Holding Co as dividends was also exempt from tax.

The lesson of the above is that in case of selling a company, it is definitely worth to check during the restructuring whether there is an entity somewhere in the ownership structure that can be used to reduce tax liabilities.

Conclusion

With the above structure capital gains realized on the sale of EU Target Co are tax free in Hungary. As the HU Holding Co pays its profit as dividend it might also be tax free on the EU Holding Co level. The only expectation is the one-year holding period, which should be considered during tax planning.

Pro Tip: firms having interest in such a structure, set up of an “empty box structure” to start the holding period might be worth to consider as it might also be available during tax planning (maintenance costs of the empty box is immaterial).

However, we should emphasize the need for careful consideration, to consult with advisors and legal experts and to discuss the planned transactions with the tax authorities.

Global 100 – 2026 for the category of: Tax Law Lawyer of the Year – Hungary

M&A Today – Global Awards 2026 for Tax Law Lawyer of the Year – Hungary

We are proud member of United Tax Network:

We are proud member of CBA Associates:

Download Tax Highlights, Hungary, 2025

Send download link to: